Lead Frame Market to Reach USD 4.98 Billion by 2032 | Growing Demand from Semiconductor Packaging & Electronics Industry

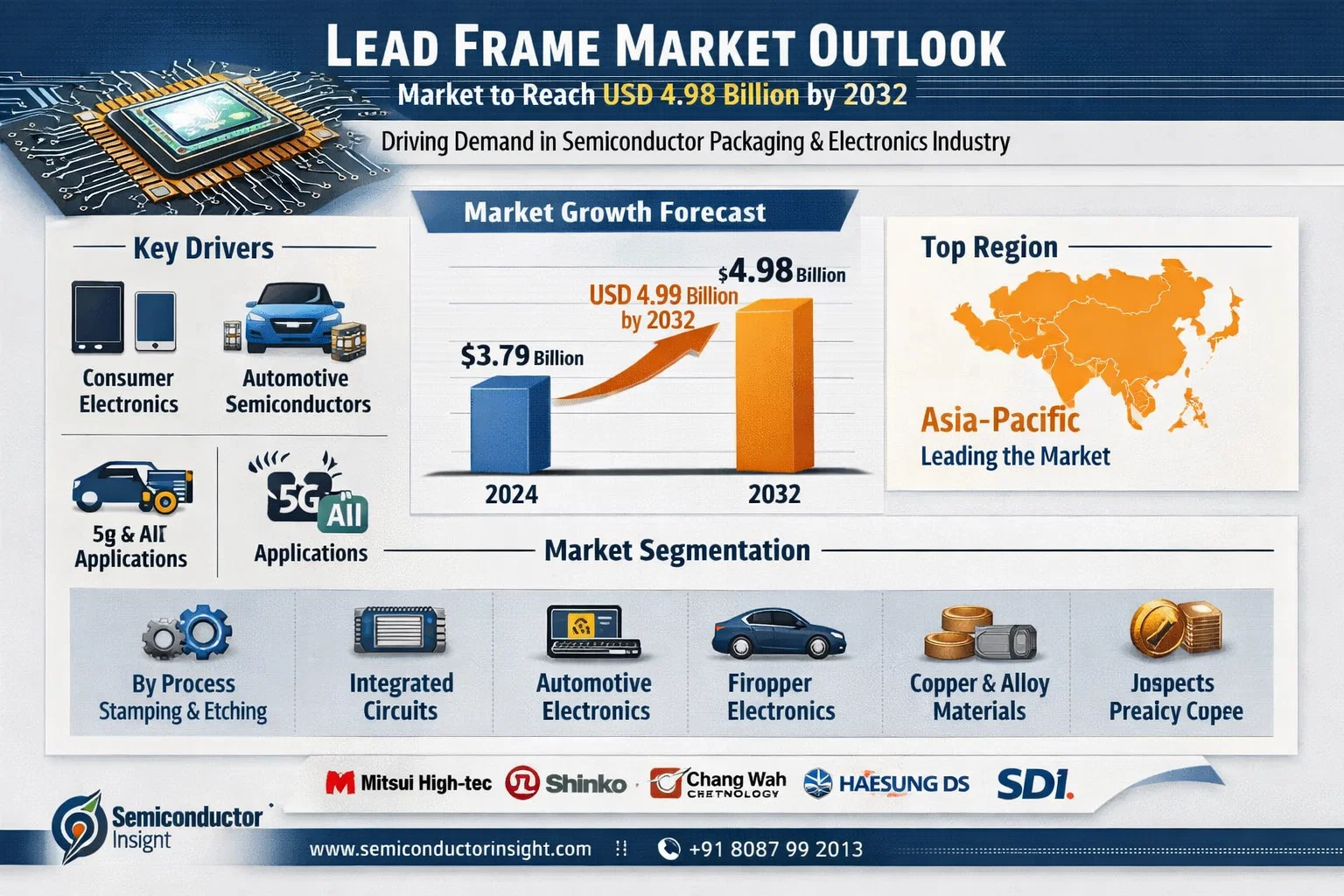

The global Lead Frame Market, valued at a robust USD 3.79 billion in 2024, is on a steady growth trajectory, projected to reach USD 4.98 billion by 2032. This expansion, representing a compound annual growth rate (CAGR) of 4.1%, is detailed in a comprehensive new report published by Semiconductor Insight. The study underscores the indispensable role of these critical components in semiconductor packaging, highlighting their function as the foundational metal structures that provide mechanical support, electrical connectivity, and heat dissipation for integrated circuits and discrete devices.

Lead frames, the metallic skeletons upon which semiconductor dies are mounted and connected, are paramount to the performance and longevity of virtually all electronic devices. Their design directly influences factors such as signal integrity, thermal management, and overall package form factor. As semiconductor technology continues its relentless march towards miniaturization and higher performance, the demand for advanced lead frames with finer pitches and enhanced materials is intensifying.

Download FREE Sample Report:

Lead Frame Market - View in Detailed Research Report

Proliferation of Electronics and Automotive Semiconductor Demand: Primary Growth Engines

The report identifies the ubiquitous expansion of the global electronics sector as the paramount driver for lead frame demand. The correlation is direct and substantial, with the integrated circuit application segment constituting the largest downstream application for lead frames. The consumer electronics segment, in particular, creates a massive and consistent demand for lead frames, driven by relentless innovation and high-volume production cycles for smartphones, laptops, and wearables.

"The Asia-Pacific region is the undisputed epicenter of the global lead frame market, accounting for a dominant share of both production and consumption," the report states. This concentration is fueled by the region's unparalleled electronics manufacturing ecosystem, which encompasses everything from semiconductor fabrication and assembly to final product assembly. With extensive supply chains for key raw materials like copper alloy and a highly skilled workforce, Asia-Pacific producers are exceptionally well-positioned to meet the evolving demands of the global semiconductor industry, particularly as packaging technologies advance to support devices for 5G, AI, and automotive applications.

Read Full Report: https://semiconductorinsight.com/report/lead-frame-market/

Market Segmentation: Stamping Process and Integrated Circuit Applications Dominate

The report provides a detailed segmentation analysis, offering a clear view of the market structure and key growth segments:

Segment Analysis:

By Process

Stamping Process Leadframe

Etching Process Leadframe

By Application

Integrated Circuit

Discrete Device

Others

By End User

Consumer Electronics

Automotive Industry

Industrial & Telecommunication

By Material

Copper Alloy

Alloy 42

Other Specialty Alloys

Download Sample Report: https://semiconductorinsight.com/download-sample-report/?product_id=127113

Competitive Landscape: Key Players and Strategic Focus

The report profiles key industry players, including:

Mitsui High-tec (Japan)

Shinko Electric Industries Co., Ltd. (Japan)

Chang Wah Technology Co., Ltd. (Taiwan)

Advanced Assembly Materials International Ltd. (AAMI) (Hong Kong)

HAESUNG DS Co., Ltd. (South Korea)

SDI (South Korea)

Fusheng Electronics (Taiwan)

Enomoto Co., Ltd. (Japan)

Kangqiang Electronics (China)

POSSEHL (Germany)

JIH LIN TECHNOLOGY CO., LTD. (Taiwan)

Jentech Precision Industrial Co., Ltd. (Taiwan)

Hualong (China)

Dynacraft Industries (India)

QPL Limited (Hong Kong)

These companies are focusing on technological advancements, such as developing lead frames for advanced packaging like QFN and QFP, and expanding production capacity in high-growth regions like Southeast Asia to capitalize on the shifting global supply chain and increasing demand.

Emerging Opportunities in Advanced Packaging and Automotive Electrification

Beyond traditional consumer electronics drivers, the report outlines significant emerging opportunities. The rapid expansion of electric vehicle (EV) production and the integration of advanced driver-assistance systems (ADAS) present substantial new growth avenues, requiring high-reliability lead frames for power semiconductors and sensors. The transition to more complex semiconductor packages for high-performance computing and 5G infrastructure, which demand lead frames with superior electrical and thermal characteristics, represents another key trend. The ongoing industry-wide push for supply chain resilience and localized manufacturing is also prompting strategic investments and partnerships within the lead frame sector, creating new competitive dynamics.

Report Scope and Availability

The market research report offers a comprehensive analysis of the global and regional Lead Frame markets from 2025–2032. It provides detailed segmentation, market size forecasts, competitive intelligence, technology trends, and an evaluation of key market dynamics.

For a detailed analysis of market drivers, restraints, opportunities, and the competitive strategies of key players, access the complete report.

Read Full Report: https://semiconductorinsight.com/report/lead-frame-market/

Download Sample Report: https://semiconductorinsight.com/download-sample-report/?product_id=127113

Get Full Report Here:

Lead Frame Market, Global Business Strategies 2025-2032 - View in Detailed Research Report

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high-technology industries. Our in-depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high-quality, data-driven research to our clients worldwide.

Website: https://semiconductorinsight.com/

International: +91 8087 99 2013

LinkedIn: Follow Us

#LeadFrameMarket

#SemiconductorPackaging

#SemiconductorIndustry

#ElectronicsManufacturing

#IntegratedCircuits

#AutomotiveSemiconductors

#EVTechnology

#5GTechnology

#AdvancedPackaging

#MarketGrowth

#ElectronicsIndustry

#AIandSemiconductors

#ChipPackaging

#IndustrialElectronics

#SemiconductorInsight

The global Lead Frame Market, valued at a robust USD 3.79 billion in 2024, is on a steady growth trajectory, projected to reach USD 4.98 billion by 2032. This expansion, representing a compound annual growth rate (CAGR) of 4.1%, is detailed in a comprehensive new report published by Semiconductor Insight. The study underscores the indispensable role of these critical components in semiconductor packaging, highlighting their function as the foundational metal structures that provide mechanical support, electrical connectivity, and heat dissipation for integrated circuits and discrete devices.

Lead frames, the metallic skeletons upon which semiconductor dies are mounted and connected, are paramount to the performance and longevity of virtually all electronic devices. Their design directly influences factors such as signal integrity, thermal management, and overall package form factor. As semiconductor technology continues its relentless march towards miniaturization and higher performance, the demand for advanced lead frames with finer pitches and enhanced materials is intensifying.

Download FREE Sample Report:

Lead Frame Market - View in Detailed Research Report

Proliferation of Electronics and Automotive Semiconductor Demand: Primary Growth Engines

The report identifies the ubiquitous expansion of the global electronics sector as the paramount driver for lead frame demand. The correlation is direct and substantial, with the integrated circuit application segment constituting the largest downstream application for lead frames. The consumer electronics segment, in particular, creates a massive and consistent demand for lead frames, driven by relentless innovation and high-volume production cycles for smartphones, laptops, and wearables.

"The Asia-Pacific region is the undisputed epicenter of the global lead frame market, accounting for a dominant share of both production and consumption," the report states. This concentration is fueled by the region's unparalleled electronics manufacturing ecosystem, which encompasses everything from semiconductor fabrication and assembly to final product assembly. With extensive supply chains for key raw materials like copper alloy and a highly skilled workforce, Asia-Pacific producers are exceptionally well-positioned to meet the evolving demands of the global semiconductor industry, particularly as packaging technologies advance to support devices for 5G, AI, and automotive applications.

Read Full Report: https://semiconductorinsight.com/report/lead-frame-market/

Market Segmentation: Stamping Process and Integrated Circuit Applications Dominate

The report provides a detailed segmentation analysis, offering a clear view of the market structure and key growth segments:

Segment Analysis:

By Process

Stamping Process Leadframe

Etching Process Leadframe

By Application

Integrated Circuit

Discrete Device

Others

By End User

Consumer Electronics

Automotive Industry

Industrial & Telecommunication

By Material

Copper Alloy

Alloy 42

Other Specialty Alloys

Download Sample Report: https://semiconductorinsight.com/download-sample-report/?product_id=127113

Competitive Landscape: Key Players and Strategic Focus

The report profiles key industry players, including:

Mitsui High-tec (Japan)

Shinko Electric Industries Co., Ltd. (Japan)

Chang Wah Technology Co., Ltd. (Taiwan)

Advanced Assembly Materials International Ltd. (AAMI) (Hong Kong)

HAESUNG DS Co., Ltd. (South Korea)

SDI (South Korea)

Fusheng Electronics (Taiwan)

Enomoto Co., Ltd. (Japan)

Kangqiang Electronics (China)

POSSEHL (Germany)

JIH LIN TECHNOLOGY CO., LTD. (Taiwan)

Jentech Precision Industrial Co., Ltd. (Taiwan)

Hualong (China)

Dynacraft Industries (India)

QPL Limited (Hong Kong)

These companies are focusing on technological advancements, such as developing lead frames for advanced packaging like QFN and QFP, and expanding production capacity in high-growth regions like Southeast Asia to capitalize on the shifting global supply chain and increasing demand.

Emerging Opportunities in Advanced Packaging and Automotive Electrification

Beyond traditional consumer electronics drivers, the report outlines significant emerging opportunities. The rapid expansion of electric vehicle (EV) production and the integration of advanced driver-assistance systems (ADAS) present substantial new growth avenues, requiring high-reliability lead frames for power semiconductors and sensors. The transition to more complex semiconductor packages for high-performance computing and 5G infrastructure, which demand lead frames with superior electrical and thermal characteristics, represents another key trend. The ongoing industry-wide push for supply chain resilience and localized manufacturing is also prompting strategic investments and partnerships within the lead frame sector, creating new competitive dynamics.

Report Scope and Availability

The market research report offers a comprehensive analysis of the global and regional Lead Frame markets from 2025–2032. It provides detailed segmentation, market size forecasts, competitive intelligence, technology trends, and an evaluation of key market dynamics.

For a detailed analysis of market drivers, restraints, opportunities, and the competitive strategies of key players, access the complete report.

Read Full Report: https://semiconductorinsight.com/report/lead-frame-market/

Download Sample Report: https://semiconductorinsight.com/download-sample-report/?product_id=127113

Get Full Report Here:

Lead Frame Market, Global Business Strategies 2025-2032 - View in Detailed Research Report

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high-technology industries. Our in-depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high-quality, data-driven research to our clients worldwide.

Website: https://semiconductorinsight.com/

International: +91 8087 99 2013

LinkedIn: Follow Us

#LeadFrameMarket

#SemiconductorPackaging

#SemiconductorIndustry

#ElectronicsManufacturing

#IntegratedCircuits

#AutomotiveSemiconductors

#EVTechnology

#5GTechnology

#AdvancedPackaging

#MarketGrowth

#ElectronicsIndustry

#AIandSemiconductors

#ChipPackaging

#IndustrialElectronics

#SemiconductorInsight

Lead Frame Market to Reach USD 4.98 Billion by 2032 | Growing Demand from Semiconductor Packaging & Electronics Industry

The global Lead Frame Market, valued at a robust USD 3.79 billion in 2024, is on a steady growth trajectory, projected to reach USD 4.98 billion by 2032. This expansion, representing a compound annual growth rate (CAGR) of 4.1%, is detailed in a comprehensive new report published by Semiconductor Insight. The study underscores the indispensable role of these critical components in semiconductor packaging, highlighting their function as the foundational metal structures that provide mechanical support, electrical connectivity, and heat dissipation for integrated circuits and discrete devices.

Lead frames, the metallic skeletons upon which semiconductor dies are mounted and connected, are paramount to the performance and longevity of virtually all electronic devices. Their design directly influences factors such as signal integrity, thermal management, and overall package form factor. As semiconductor technology continues its relentless march towards miniaturization and higher performance, the demand for advanced lead frames with finer pitches and enhanced materials is intensifying.

Download FREE Sample Report:

Lead Frame Market - View in Detailed Research Report

Proliferation of Electronics and Automotive Semiconductor Demand: Primary Growth Engines

The report identifies the ubiquitous expansion of the global electronics sector as the paramount driver for lead frame demand. The correlation is direct and substantial, with the integrated circuit application segment constituting the largest downstream application for lead frames. The consumer electronics segment, in particular, creates a massive and consistent demand for lead frames, driven by relentless innovation and high-volume production cycles for smartphones, laptops, and wearables.

"The Asia-Pacific region is the undisputed epicenter of the global lead frame market, accounting for a dominant share of both production and consumption," the report states. This concentration is fueled by the region's unparalleled electronics manufacturing ecosystem, which encompasses everything from semiconductor fabrication and assembly to final product assembly. With extensive supply chains for key raw materials like copper alloy and a highly skilled workforce, Asia-Pacific producers are exceptionally well-positioned to meet the evolving demands of the global semiconductor industry, particularly as packaging technologies advance to support devices for 5G, AI, and automotive applications.

Read Full Report: https://semiconductorinsight.com/report/lead-frame-market/

Market Segmentation: Stamping Process and Integrated Circuit Applications Dominate

The report provides a detailed segmentation analysis, offering a clear view of the market structure and key growth segments:

Segment Analysis:

By Process

Stamping Process Leadframe

Etching Process Leadframe

By Application

Integrated Circuit

Discrete Device

Others

By End User

Consumer Electronics

Automotive Industry

Industrial & Telecommunication

By Material

Copper Alloy

Alloy 42

Other Specialty Alloys

Download Sample Report: https://semiconductorinsight.com/download-sample-report/?product_id=127113

Competitive Landscape: Key Players and Strategic Focus

The report profiles key industry players, including:

Mitsui High-tec (Japan)

Shinko Electric Industries Co., Ltd. (Japan)

Chang Wah Technology Co., Ltd. (Taiwan)

Advanced Assembly Materials International Ltd. (AAMI) (Hong Kong)

HAESUNG DS Co., Ltd. (South Korea)

SDI (South Korea)

Fusheng Electronics (Taiwan)

Enomoto Co., Ltd. (Japan)

Kangqiang Electronics (China)

POSSEHL (Germany)

JIH LIN TECHNOLOGY CO., LTD. (Taiwan)

Jentech Precision Industrial Co., Ltd. (Taiwan)

Hualong (China)

Dynacraft Industries (India)

QPL Limited (Hong Kong)

These companies are focusing on technological advancements, such as developing lead frames for advanced packaging like QFN and QFP, and expanding production capacity in high-growth regions like Southeast Asia to capitalize on the shifting global supply chain and increasing demand.

Emerging Opportunities in Advanced Packaging and Automotive Electrification

Beyond traditional consumer electronics drivers, the report outlines significant emerging opportunities. The rapid expansion of electric vehicle (EV) production and the integration of advanced driver-assistance systems (ADAS) present substantial new growth avenues, requiring high-reliability lead frames for power semiconductors and sensors. The transition to more complex semiconductor packages for high-performance computing and 5G infrastructure, which demand lead frames with superior electrical and thermal characteristics, represents another key trend. The ongoing industry-wide push for supply chain resilience and localized manufacturing is also prompting strategic investments and partnerships within the lead frame sector, creating new competitive dynamics.

Report Scope and Availability

The market research report offers a comprehensive analysis of the global and regional Lead Frame markets from 2025–2032. It provides detailed segmentation, market size forecasts, competitive intelligence, technology trends, and an evaluation of key market dynamics.

For a detailed analysis of market drivers, restraints, opportunities, and the competitive strategies of key players, access the complete report.

Read Full Report: https://semiconductorinsight.com/report/lead-frame-market/

Download Sample Report: https://semiconductorinsight.com/download-sample-report/?product_id=127113

Get Full Report Here:

Lead Frame Market, Global Business Strategies 2025-2032 - View in Detailed Research Report

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high-technology industries. Our in-depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high-quality, data-driven research to our clients worldwide.

🌐 Website: https://semiconductorinsight.com/

📞 International: +91 8087 99 2013

🔗 LinkedIn: Follow Us

#LeadFrameMarket

#SemiconductorPackaging

#SemiconductorIndustry

#ElectronicsManufacturing

#IntegratedCircuits

#AutomotiveSemiconductors

#EVTechnology

#5GTechnology

#AdvancedPackaging

#MarketGrowth

#ElectronicsIndustry

#AIandSemiconductors

#ChipPackaging

#IndustrialElectronics

#SemiconductorInsight

0 Maoni

0 Shiriki

533 Mitazamo

0 Hakiki