Polyurethane Market Grows from USD 38,990 Million to USD 50,540 Million by 2030

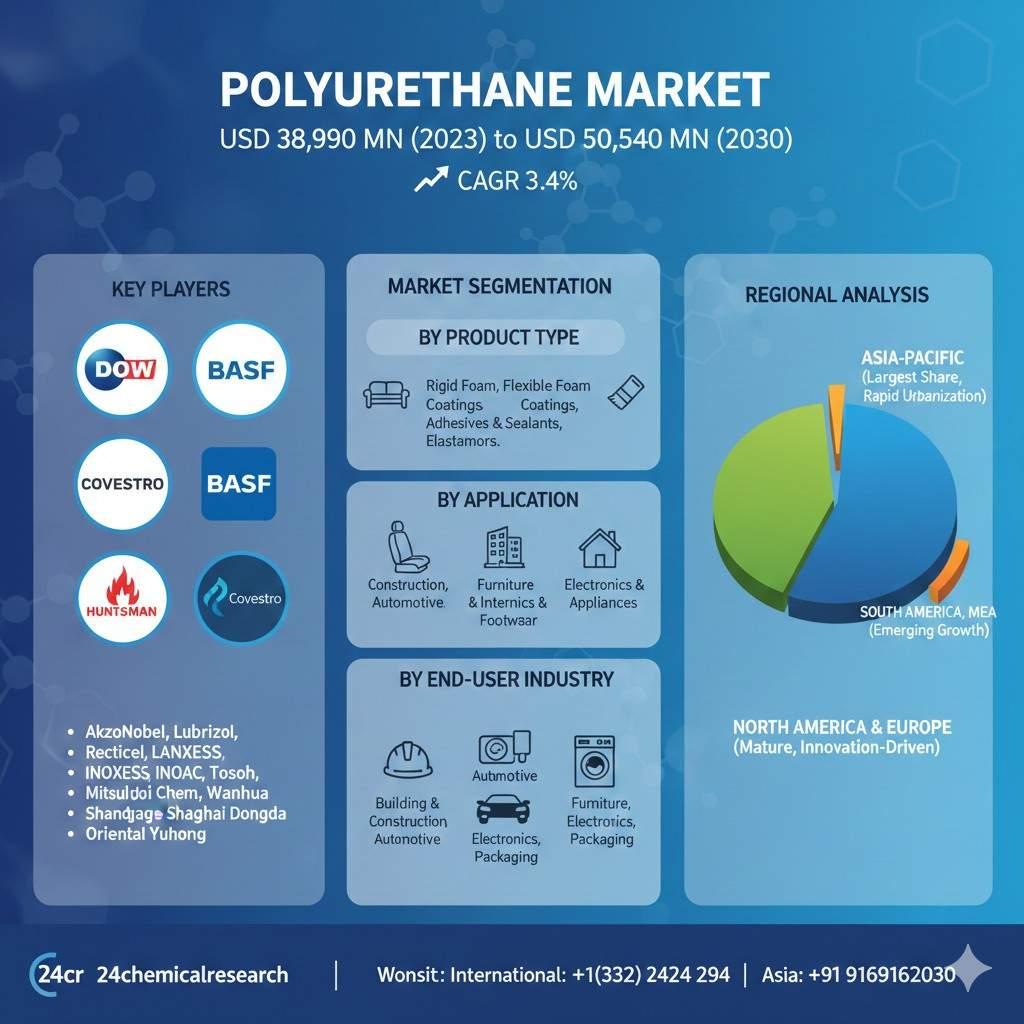

Global Polyurethane (PU) market was valued at USD 38,990 million in 2023 and is projected to reach USD 50,540 million by 2030, exhibiting a steady CAGR of 3.4% during the forecast period.

Polyurethane, a remarkably versatile polymer created through the reaction of polyols with diisocyanates, has firmly established itself as a foundational material across the global industrial landscape. Its unique characteristic the ability to be engineered into an incredibly wide range of forms including flexible and rigid foams, coatings, adhesives, sealants, and elastomers (often referred to as CASE applications) makes it indispensable. This chameleon-like quality allows PU to provide tailored solutions for everything from the cushioning in your car seat to the insulation keeping buildings energy-efficient. Its excellent durability, abrasion resistance, and versatility ensure its continued relevance amidst evolving material demands.

Get Full Report Here: https://www.24chemicalresearch.com/reports/262582/global-polyurethane-market-2024-2030-311

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities.

Powerful Market Drivers Propelling Expansion

- Surging Demand from the Construction Industry: The construction sector remains the single largest consumer of polyurethane, particularly rigid foams used for insulation. The global push for energy efficiency, driven by stringent building codes and a growing focus on sustainability, is a massive growth vector. Polyurethane insulation boards and spray foam can reduce energy consumption for heating and cooling by up to 40-50% compared to traditional materials. With the global construction market expected to reach over $15 trillion by 2030, the demand for high-performance insulation materials like PU is set to grow relentlessly, especially in emerging economies undergoing rapid urbanization.

- Automotive Lightweighting and Interior Comfort: The automotive industry's relentless pursuit of lightweighting to meet fuel efficiency and emission standards heavily relies on polyurethane. It is used in lightweight seats, instrument panels, and interior headliners. Furthermore, the rise of electric vehicles (EVs) presents a new frontier, where PU is critical for battery pack encapsulation, providing excellent thermal management and protection. Beyond structure, consumer demand for enhanced comfort drives the use of high-resilience flexible foams in seating, making the automotive sector a consistent and evolving consumer.

- Innovation in Appliances and Consumer Goods: Polyurethane's excellent thermal insulating properties make it the material of choice for refrigerators, freezers, and water heaters globally. As appliance energy ratings become stricter and consumers demand more efficient products, the use of optimized PU foams is intensifying. Beyond appliances, PU is ubiquitous in furniture (cushioning), footwear (shoe soles), and bedding (mattresses), sectors that benefit directly from rising disposable incomes and urbanization, particularly in the Asia-Pacific region.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/262582/global-polyurethane-market-2024-2030-311

Significant Market Restraints Challenging Adoption

Despite its widespread use, the market faces hurdles that must be overcome to ensure sustainable long-term growth.

- Volatility in Raw Material Prices: The production of polyurethane is heavily dependent on crude oil derivatives, specifically propylene and ethylene for polyols, and aromatic isocyanates like MDI and TDI. Fluctuations in crude oil prices, which can swing by 20-30% annually, directly impact the cost structure of PU manufacturers. This volatility creates significant pricing uncertainty for downstream industries and can compress profit margins, making long-term planning and budgeting a considerable challenge for market participants.

- Environmental and Health Regulations: Stringent global regulations concerning the use of certain isocyanates, which are respiratory sensitizers, necessitate significant investment in workplace safety and handling procedures. Furthermore, regulations like the EU's REACH and the increasing global scrutiny on flame retardants used in PU foams add layers of compliance complexity. The industry is also under pressure regarding the end-of-life phase of PU products, particularly non-recyclable foams, pushing the need for more circular economy solutions.

Critical Market Challenges Requiring Innovation

The transition towards a more sustainable future presents its own set of challenges for the established polyurethane industry. The development and commercialization of bio-based polyols derived from soy, castor oil, or other renewable sources, while promising, currently face hurdles related to scalability and cost-competitiveness with their petrochemical counterparts. Achieving consistent performance and properties at a commercial scale with bio-based feedstocks remains a key R&D focus.

Additionally, improving the recyclability of polyurethane products is a major technical challenge. While mechanical and chemical recycling pathways exist, they are not yet economically viable or widely adopted for the vast majority of PU waste. Overcoming the technical barriers to create a truly circular model for PU, from production to post-consumer waste, is critical for the industry's social license to operate in an increasingly eco-conscious world. The fragmented nature of the supply chain, from raw material producers to numerous downstream applicators, also complicates the implementation of industry-wide sustainability initiatives.

Vast Market Opportunities on the Horizon

- The Rise of Bio-based and Circular Polyurethanes: This represents the most significant long-term opportunity. Consumer and brand owner demand for sustainable materials is creating a fertile ground for bio-based PU. Advancements in green chemistry are leading to polyols with bio-content exceeding 20-30%, which are increasingly being adopted in automotive interiors, footwear, and packaging. The development of chemical recycling technologies that can break down PU waste back into its original polyol components could revolutionize the industry, creating a closed-loop system and mitigating end-of-life concerns.

- Advanced Applications in Electronics and Medical Devices: Polyurethane is finding new, high-value applications. In electronics, durable and flexible PU coatings are essential for protecting wearable devices and cables. In the medical field, its biocompatibility makes it suitable for a range of devices, including catheter tubing, wound dressings, and tissue engineering scaffolds. The stringent performance requirements in these sectors command premium prices and open new growth avenues beyond traditional markets.

- Strategic Partnerships for Innovation and Sustainability: The market is witnessing increased collaboration across the value chain. Chemical giants are partnering with automotive OEMs to co-develop lightweighting solutions, and raw material producers are working with waste management companies to pioneer recycling technologies. These alliances are crucial for pooling R&D resources, sharing risks, and accelerating the development of next-generation, sustainable PU products that meet the complex demands of modern industry.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Product Type:

The market is segmented into Rigid Foam, Flexible Foam, Coatings, Adhesives & Sealants, Elastomers, and others. Flexible Foam historically holds a dominant share, driven by its extensive use in furniture, bedding, and automotive interiors. However, the Rigid Foam segment is witnessing robust growth, fueled by the global construction boom and the escalating demand for energy-efficient insulation materials in both residential and commercial buildings.

By Application:

Application segments include Furniture & Interiors, Construction, Electronics & Appliances, Automotive, Footwear, and others. The Construction sector is the largest application area, leveraging PU's superior insulating properties. The Automotive segment follows closely, utilizing PU for a multitude of components from seating and dashboards to insulation and noise dampening, with its role in electric vehicles representing a significant growth frontier.

By End-User Industry:

The end-user landscape includes Building & Construction, Automotive, Furniture, Electronics, Footwear, and Packaging. The Building & Construction industry accounts for the major share, a testament to PU's critical role in modern infrastructure. The Automotive industry is a key consumer, with its continuous innovation in vehicle design and the shift towards EVs ensuring sustained demand for advanced polyurethane solutions.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/262582/global-polyurethane-market-2024-2030-311

Competitive Landscape:

The global Polyurethane market is highly consolidated and characterized by the dominance of a few major chemical conglomerates. The top three companies—BASF (Germany), Dow (U.S.), and Covestro (Germany)—collectively command a significant portion of the global market share. Their leadership is underpinned by massive, integrated production facilities, extensive research and development capabilities focused on product innovation and sustainability, and a strong global distribution network that serves a diverse range of industries.

List of Key Polyurethane Companies Profiled:

● Dow (U.S.)

● BASF (Germany)

● Huntsman (U.S.)

● AkzoNobel (Netherlands)

● Covestro (Germany)

● Lubrizol (U.S.)

● Recticel (Belgium)

● LANXESS (Germany)

● INOAC (Japan)

● Tosoh (Japan)

● Mitsui Chem (Japan)

● Woodbridge Foam (Canada)

● Wanhua (China)

● Shanghai Dongda (China)

● Oriental Yuhong (China)

The competitive strategy is overwhelmingly focused on expanding production capacity, developing sustainable product lines (e.g., bio-based or recyclable PU), and forming deep, collaborative partnerships with key end-users in the automotive and construction industries to create tailored solutions and secure long-term supply agreements.

Regional Analysis: A Global Footprint with Distinct Leaders

● Asia-Pacific: Is the undisputed leader, holding the largest share of the global market. This dominance is fueled by massive industrialization, rapid urbanization, and a booming construction sector, particularly in China and India. The region is both the largest producer and consumer of polyurethane, supported by a strong manufacturing base for end-use industries like appliances, automotive, and footwear.

● North America and Europe: Together, they form the mature yet innovation-driven markets. These regions are characterized by stringent energy efficiency regulations that drive demand for high-performance PU insulation in construction. The presence of major automotive OEMs and a strong focus on sustainability and bio-based materials keep these regions at the forefront of advanced PU application development.

● South America, and Middle East & Africa: These regions represent the emerging growth frontiers of the PU market. While currently smaller in scale, they present significant long-term growth opportunities driven by increasing investments in infrastructure development, growing automotive production, and rising consumer purchasing power.

Get Full Report Here: https://www.24chemicalresearch.com/reports/262582/global-polyurethane-market-2024-2030-311

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/262582/global-polyurethane-market-2024-2030-311

Other related reports:

Sodium Benzenesulfinate Market, Global Outlook and Forecast 2023-2029

Southeast Asia 2-Nitroaniline Market Outlook and Forecast 2025-2032

Smart Nanomaterials Market, Global Outlook and Forecast 2025-2031

Southeast Asia Brominated Flame Retardants Market Outlook and Forecast 2025-2032

Middle East Lead Vinyl Sheets Market Research Report 2024-2030

Southeast Asia Fumaric Acid Monoethyl Ester (MEF) Market Outlook and Forecast 2024-2030

Dinotefuran Market, Global Outlook and Forecast 2025-2032

Monoethanolamine Market Research Report 2025,Global Forecast to 2032

Contact us

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/

Follow us on LinkedIn: https://www.linkedin.com/company/24chemicalresearch