High Purity Antimony Metal Market Report 2026–2034: Growth, Demand & Future Opportunities

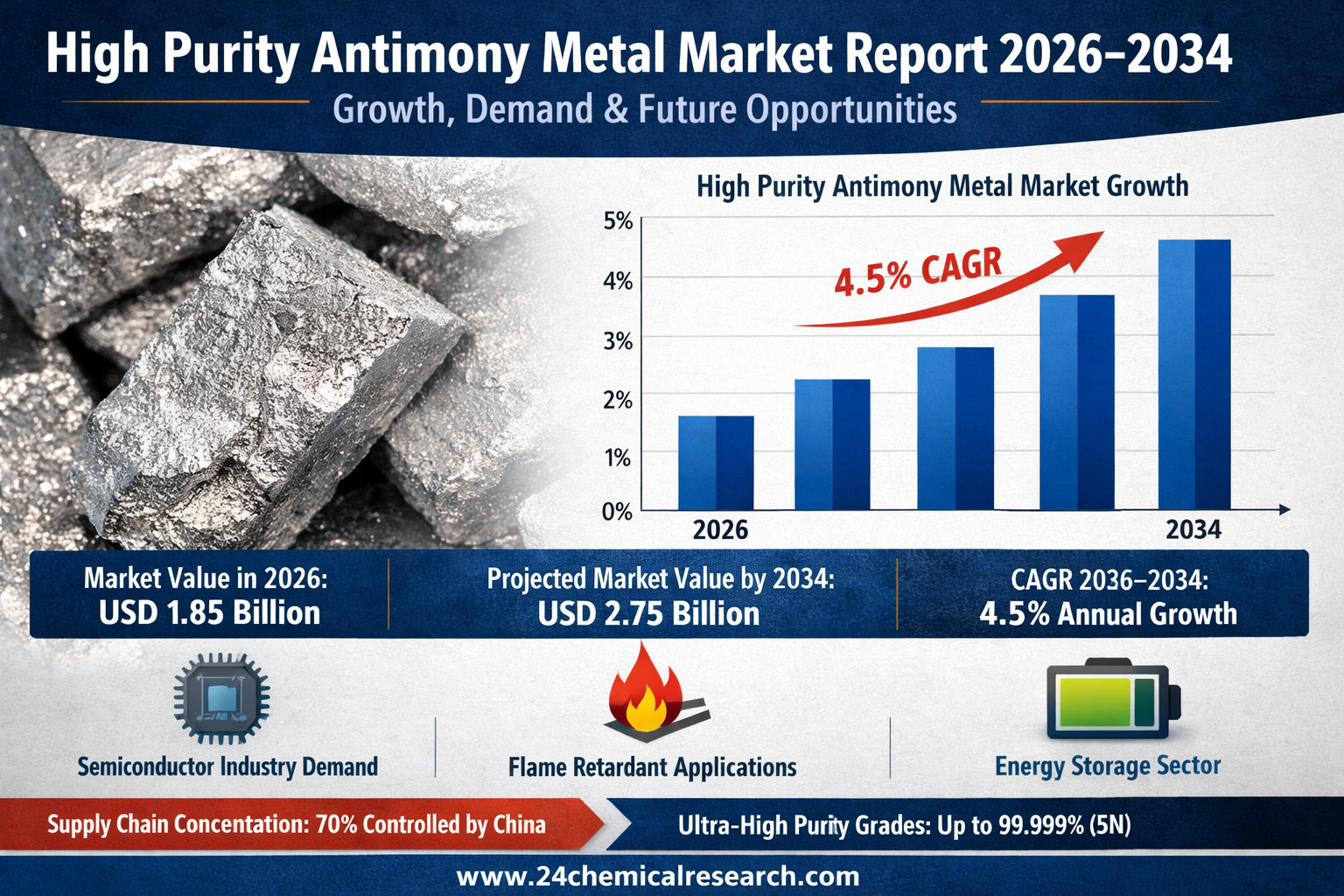

Global High Purity Antimony Metal Market was valued at USD 1.85 billion in 2026 and is projected to reach USD 2.75 billion by 2034, exhibiting a compound annual growth rate (CAGR) of 4.5% during the forecast period.

High purity antimony metal, typically defined as material with purity levels of 99.5% (2N5) or higher, has transitioned from a niche industrial material to a critical component in advanced technological applications. Its unique properties—including exceptional hardening capabilities, semiconductor characteristics, and thermal stability—make it indispensable across multiple high-tech sectors. The material is commercially available in various grades such as 3N (99.9%), 4N (99.99%), 4.5N (99.995%), and 5N (99.999%), with higher purity grades commanding significant price premiums due to their specialized production requirements and superior performance characteristics.

Get Full Report Here: https://www.24chemicalresearch.com/reports/307148/high-purity-antimony-metal-market

Market Dynamics:

The market's evolution is characterized by a complex interplay of growth drivers, persistent challenges, and emerging opportunities that collectively shape its trajectory.

Powerful Market Drivers Propelling Expansion

-

Electronics and Semiconductor Industry Demand: The integration of high purity antimony in semiconductor manufacturing represents a primary growth vector, particularly for doping applications in silicon wafers and production of infrared detectors. The global semiconductor industry, valued at approximately $600 billion, continuously seeks materials that enhance device performance and enable miniaturization. Antimony's role in improving electron mobility and thermal stability makes it crucial for next-generation electronic devices. Furthermore, the expansion of 5G infrastructure and Internet of Things (IoT) devices creates sustained demand for antimony-based components, particularly in high-frequency applications where material purity directly impacts performance.

-

Flame Retardant Applications: Antimony trioxide, derived from high purity antimony metal, serves as an essential synergist in halogenated flame retardants. With global fire safety regulations becoming increasingly stringent across construction, transportation, and electronics sectors, demand for effective flame suppression materials continues to rise. The global flame retardants market, projected to exceed $12 billion by 2030, relies heavily on antimony-based formulations that demonstrate 20-30% greater efficacy compared to alternative solutions. This application segment provides stable, consistent demand despite growing environmental concerns about halogenated compounds.

-

Energy Storage Innovations: While lithium-ion technology dominates portable electronics, lead-acid batteries utilizing antimony-hardened grids remain crucial for automotive starting systems and industrial energy storage. The exceptional deep-cycle performance and durability of antimony-enhanced batteries make them indispensable for applications requiring reliable power delivery under demanding conditions. Recent advancements in battery technology have demonstrated that antimony additives can improve cycle life by 15-25% in industrial applications, ensuring continued relevance despite competition from newer technologies.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/307148/high-purity-antimony-metal-market

Significant Market Restraints Challenging Adoption

Despite its critical applications, the market faces substantial hurdles that limit its growth potential and create operational challenges.

-

Supply Chain Concentration Risks: The market suffers from extreme geographic concentration, with China controlling approximately 70% of global antimony production and refining capacity. This dominance creates vulnerability for downstream industries, exposing them to geopolitical tensions, export restrictions, and price manipulation. Recent trade policy fluctuations have demonstrated how quickly supply disruptions can occur, with price volatility reaching 25-40% during periods of export constraint. This concentration discourages long-term investment in antimony-dependent technologies among Western manufacturers seeking supply chain stability.

-

Environmental and Regulatory Pressures: Antimony mining and processing face increasing environmental scrutiny due to the potential toxicity of mining byproducts and processing waste. Compliance costs have risen 15-20% annually in major producing regions as regulations tighten. In the European Union and North America, the classification of antimony as a substance of very high concern under REACH regulations creates additional compliance burdens. Environmental impact assessments for new mining operations now typically require 24-36 months for approval, significantly delaying capacity expansion projects.

Critical Market Challenges Requiring Innovation

The transition from traditional applications to high-tech uses presents unique challenges that demand innovative solutions and substantial investment.

Production of ultra-high purity antimony (4N and above) requires sophisticated refining techniques that are both energy-intensive and technologically complex. Maintaining consistent quality at commercial scale remains difficult, with even advanced facilities experiencing batch-to-batch variations that can affect up to 15% of production output. The capital expenditure required for precision refining equipment represents a significant barrier to entry, with new facilities requiring investments of $50-100 million for economically viable operation.

Additionally, the market contends with persistent substitution threats across multiple applications. In flame retardants, non-halogenated alternatives are gaining market share despite performance limitations. In batteries, the shift toward lithium-ion technology continues, particularly in automotive applications where energy density outweighs durability considerations. These substitution trends require antimony producers to continuously demonstrate the superior performance characteristics and cost-effectiveness of their materials to maintain market position.

Vast Market Opportunities on the Horizon

-

Advanced Semiconductor Applications: The ongoing miniaturization of semiconductor devices creates opportunities for ultra-high purity antimony in new doping applications and compound semiconductors. Research indicates that antimony-based materials could enable next-generation transistors with improved thermal characteristics and electron mobility. The development of antimony-based thin films for photovoltaic applications represents another growth frontier, particularly in emerging photovoltaic technologies that offer improved efficiency compared to traditional silicon-based solutions.

-

Geographic Supply Diversification: The current supply concentration presents substantial opportunities for developing production capacity outside China. Countries with significant antimony resources, including Australia, Canada, and Bolivia, are attracting investment in new mining and refining projects. These developments not only reduce geopolitical risk but also create opportunities for implementing more sustainable production methods that appeal to environmentally conscious end-users. Projects incorporating advanced water recycling and waste management systems can command premium pricing while ensuring regulatory compliance.

-

Recycling and Circular Economy Initiatives: Increasing focus on material sustainability drives opportunities in antimony recycling from electronic waste and industrial byproducts. Advanced recycling technologies can recover high purity antimony from end-of-life products with recovery rates exceeding 90%, creating a secondary supply stream that reduces dependence on primary production. The development of closed-loop recycling systems represents both an environmental imperative and a significant business opportunity as manufacturers seek to demonstrate sustainability credentials to customers and regulators.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into 3N Purity, 4N Purity, 4.5N Purity, 5N Purity, and others. 4.5N Purity currently represents the most dynamic segment, offering an optimal balance between performance characteristics and production economics for semiconductor applications. This grade provides sufficient purity for most electronic applications while remaining economically viable for mass production. The 5N segment, while smaller in volume, commands significant price premiums for specialized applications where even minimal impurity levels can affect performance.

By Application:

Application segments include Electronics and Semiconductors, Flame Retardants, Lead-Acid Batteries, and others. The Electronics and Semiconductors segment demonstrates the strongest growth momentum, driven by continuous technological advancement and increasing semiconductor content across all electronic devices. While flame retardants remain the largest application by volume, the semiconductor segment offers higher growth rates and better margin potential due to the specialized nature of the required materials and the critical importance of performance characteristics.

By End-User Industry:

The end-user landscape includes Electronics Manufacturing, Automotive, Construction, and Energy Storage. The Electronics Manufacturing industry accounts for the most significant share of high purity demand, leveraging antimony's properties for semiconductor fabrication and specialized components. The Automotive sector remains important for both battery applications and flame retardant use in vehicle interiors, while the Energy Storage segment shows promising growth potential as grid storage requirements increase globally.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/307148/high-purity-antimony-metal-market

Competitive Landscape:

The global High Purity Antimony Metal market is moderately consolidated with strong competition between established producers and emerging players. The top three companies—Hunan Gold Group (China), Hsikwang Shan Twinking Star (China), and Mandalay Resources (Canada)—collectively command approximately 45% of the market share as of 2025. Their dominance is underpinned by vertical integration, extensive technical expertise, and long-term customer relationships in key end-use industries.

List of Key High Purity Antimony Metal Companies Profiled:

-

Hunan Gold Group (China)

-

Hsikwang Shan Twinking Star (China)

-

Mandalay Resources (Canada)

-

Dongfeng (China)

-

Hechi Nanfang Non-ferrous Metals Group (China)

-

GeoProMining (Russia)

-

China-Tin Group (China)

-

Anhua Huayu Antimony Industry (China)

-

Huachang Group (China)

-

Yongcheng Antimony Industry (China)

-

Geodex Minerals (Canada)

-

United States Antimony (USA)

Competitive strategy focuses heavily on technological innovation to improve purity levels and production efficiency, coupled with strategic partnerships with end-users to develop application-specific solutions. Established players are investing significantly in research and development to maintain technological leadership, while newer entrants focus on niche applications and geographic markets underserved by major producers.

Regional Analysis: A Global Footprint with Distinct Leaders

-

Asia-Pacific: Dominates the global market, holding over 70% of both production and consumption. China's position as the production hub is reinforced by extensive reserves, established infrastructure, and strong domestic demand from its electronics manufacturing sector. Japan and South Korea contribute significant demand for high purity grades for semiconductor applications, while Southeast Asian countries are emerging as important consumption centers as electronics manufacturing expands throughout the region.

-

North America: Represents the second-largest market, driven by strong demand from the semiconductor and aerospace sectors. The United States maintains strategic stockpiles of antimony, recognizing its importance for defense and critical infrastructure applications. While domestic production is limited, strong technical capabilities in purification and processing support the region's position in high-value applications. Recent initiatives to develop domestic sources reflect growing concerns about supply chain security.

-

Europe: Shows steady demand primarily from the automotive and construction sectors for flame retardant applications. The region's stringent environmental regulations drive demand for high purity materials that meet regulatory requirements while ensuring performance. Germany and France lead consumption patterns, supported by their strong chemical and automotive industries. Limited primary production capacity makes Europe heavily dependent on imports, particularly from China.

Get Full Report Here: https://www.24chemicalresearch.com/reports/307148/high-purity-antimony-metal-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/307148/high-purity-antimony-metal-market