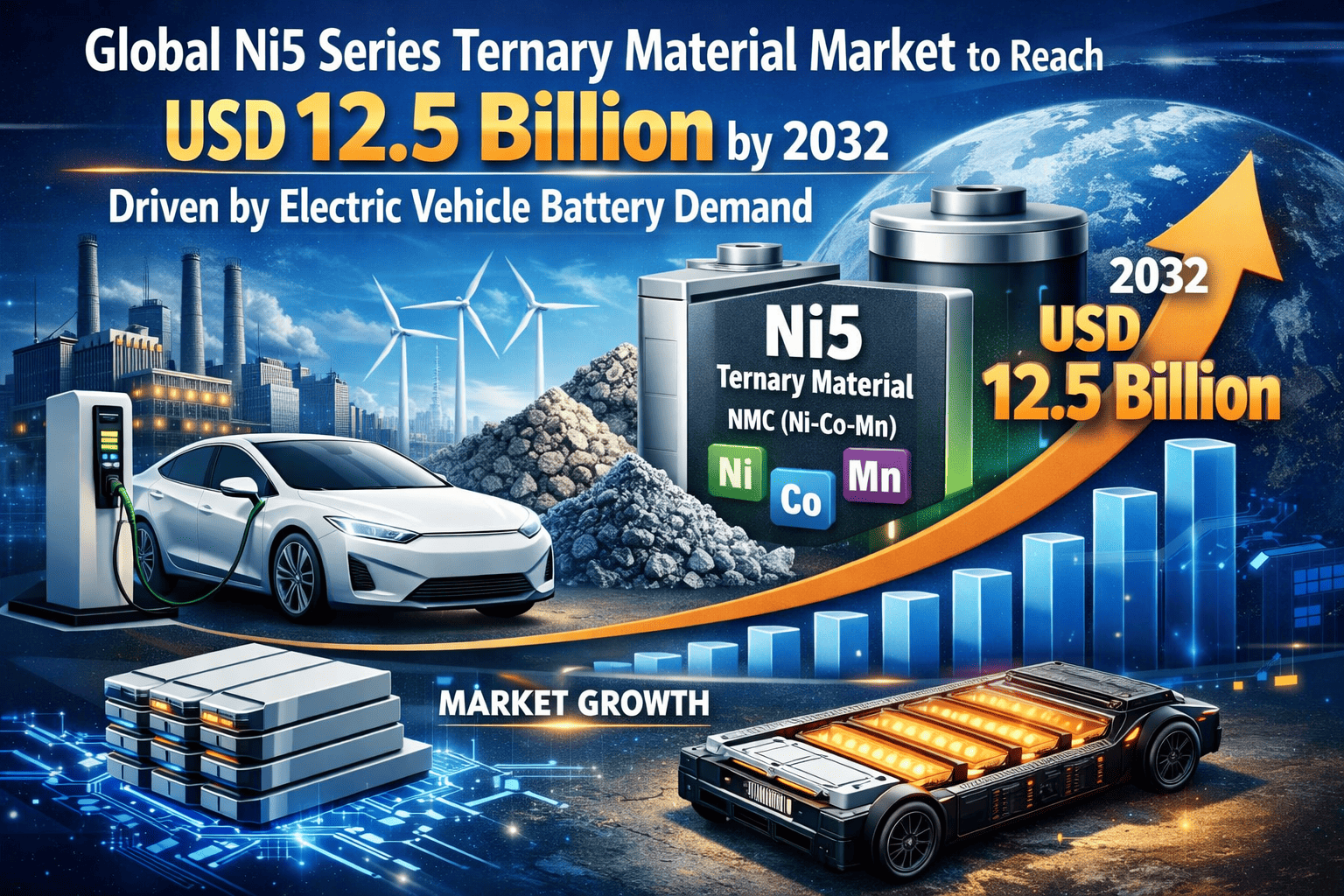

Global Ni5 Series Ternary Material Market to Reach USD 12.5 Billion by 2032 Driven by Electric Vehicle Battery Demand

Global Ni5 Series Ternary Material market was valued at USD 3.8 billion in 2024 and is projected to reach USD 12.5 billion by 2032, exhibiting a robust CAGR of 18.2% during the forecast period.

Ni5 Series Ternary Material, a high-nickel cathode chemistry composed predominantly of nickel, cobalt, and manganese (typically in ratios like 8:1:1), represents the cutting edge of lithium-ion battery technology. This advanced material has moved from laboratory development to commercial production, becoming the cornerstone of next-generation energy storage solutions. Its unique properties—including exceptional energy density, superior cycling stability, and enhanced thermal safety—make it transformative for applications demanding long-range and high-performance power. Unlike earlier cathode materials, Ni5's high nickel content enables significantly greater specific capacity while maintaining structural integrity, facilitating its integration into electric vehicles and large-scale energy storage systems.

Get Full Report Here: https://www.24chemicalresearch.com/reports/266148/global-ni-series-ternary-material-market-2024-2030-720

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities.

Powerful Market Drivers Propelling Expansion

1. Electric Vehicle Revolution Demanding Higher Energy Density: The adoption of Ni5 Series Ternary Material in electric vehicle batteries represents the dominant growth vector. The global electric vehicle market, projected to exceed 30 million units annually by 2030, requires batteries that offer extended range and faster charging capabilities. Ni5 cathodes deliver 15-25% higher energy density compared to conventional NMC 622 or NMC 811 formulations, enabling vehicles to achieve 400-600 km ranges on a single charge. Major automotive manufacturers are rapidly transitioning to high-nickel chemistries, with over 70% of new EV models announced for 2025-2026 featuring Ni5-based battery systems.

2. Grid Storage and Renewable Integration Requirements: The renewable energy sector's explosive growth is driving unprecedented demand for advanced energy storage solutions. Ni5 materials demonstrate exceptional performance in large-scale battery storage systems, particularly in frequency regulation and peak shaving applications. Their ability to maintain 80-85% capacity retention after 4,000-5,000 cycles makes them ideal for daily cycling requirements. With global energy storage deployments expected to reach 400 GWh by 2030, Ni5 chemistry is positioned to capture approximately 35% of this market segment due to its optimal balance of performance and cost.

3. Consumer Electronics Pushing Performance Boundaries: The consumer electronics industry continues to demand higher energy density in smaller form factors. Ni5 Ternary Materials enable smartphone batteries to achieve 20-30% longer runtime while maintaining the same physical dimensions. For premium laptops and portable devices, this chemistry supports all-day battery life without increasing weight. The global consumer electronics battery market, valued at over $25 billion, is rapidly adopting high-nickel cathodes, with penetration rates expected to reach 40% in premium devices by 2026.

Get Full Report Here: https://www.24chemicalresearch.com/reports/266148/global-ni-series-ternary-material-market-2024-2030-720

Significant Market Restraints Challenging Adoption

Despite its superior performance, the market faces technological and economic hurdles that must be overcome for widespread adoption.

1. Manufacturing Complexity and Elevated Production Costs: The synthesis of high-nickel ternary materials requires precise control of atmosphere and temperature during calcination, with oxygen levels maintained below 10 ppm and temperature variations kept within ±2°C. This specialized manufacturing environment increases production costs by 25-35% compared to conventional cathode materials. Additionally, the hygroscopic nature of high-nickel materials necessitates dry room conditions during processing, adding 15-20% to operational expenses and creating significant barriers for new market entrants.

2. Supply Chain Vulnerabilities and Raw Material Volatility: The dependence on high-purity nickel and cobalt creates supply chain challenges, particularly given the geographic concentration of these resources. Nickel prices have shown volatility of 30-40% annually, while cobalt prices can fluctuate up to 50% within single quarters. Recent geopolitical developments have further complicated sourcing strategies, with many manufacturers seeking to diversify their supply chains but facing 18-24 month timelines to qualify new material sources that meet the stringent purity requirements of Ni5 production.

Critical Market Challenges Requiring Innovation

The transition from pilot-scale production to mass manufacturing presents substantial technical challenges that the industry must overcome.

Maintaining consistent quality at production volumes exceeding 1,000 tons monthly proves difficult, with current processes achieving only 75-85% yield of saleable product. The material's tendency toward lithium residue formation and surface reactivity requires sophisticated washing and coating processes that add complexity to manufacturing. Furthermore, ensuring uniform particle size distribution remains problematic, with current classification methods resulting in 15-20% material loss to off-spec fractions.

Additionally, the industry faces significant technical hurdles in cell manufacturing. The high alkalinity of Ni5 materials requires specialized electrode formulations and binder systems, with current solutions adding 8-12% to electrode production costs. These challenges necessitate substantial R&D investments, typically consuming 12-18% of revenue for material producers, creating a high barrier for smaller companies seeking to enter this market.

Vast Market Opportunities on the Horizon

1. Solid-State Battery Integration: Ni5 Ternary Materials are emerging as the cathode of choice for next-generation solid-state batteries. Their compatibility with solid electrolytes demonstrates 20-30% higher energy density compared to traditional liquid electrolyte systems. Recent developments show promise for achieving 500+ Wh/kg at the cell level, potentially revolutionizing electric aviation and premium automotive applications. With solid-state battery production projected to reach 50 GWh by 2030, Ni5 materials are positioned to capture this high-value market segment.

2. Recycling and Circular Economy Initiatives: The established recycling pathways for nickel-based batteries present substantial opportunities. Advanced hydrometallurgical processes can recover over 95% of the nickel, cobalt, and manganese from spent Ni5 batteries at costs 30-40% lower than virgin material production. This circular approach not only addresses supply chain concerns but also reduces the environmental footprint of battery production by 50-60%, creating both economic and sustainability advantages.

3. Strategic Vertical Integration: The market is witnessing accelerated vertical integration, with over 40 major partnerships formed in the past two years between material producers, battery manufacturers, and automotive OEMs. These alliances are crucial for securing supply, reducing time-to-market by 30-40%, and co-developing application-specific material formulations. Recent collaborations have focused on developing cobalt-reduced or cobalt-free variants of Ni5 materials, addressing both cost and ethical sourcing concerns.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Single Crystal Ni5 Series Ternary Material and Polycrystal Ni5 Series Ternary Material. Single Crystal Ni5 Material currently leads the premium segment, favored for its superior cycling stability, reduced surface area, and enhanced safety characteristics. The polycrystal form maintains importance for applications requiring maximum energy density and lower cost positions, particularly in consumer electronics and entry-level electric vehicles.

By Application:

Application segments include Consumer Battery, Power Battery, and Energy Storage Battery. The Power Battery segment dominates the market, driven by the insatiable demand from the electric vehicle industry for higher energy density and longer cycle life. However, the Energy Storage segment is expected to exhibit the highest growth rate in the coming years as grid-scale storage projects increasingly adopt high-nickel chemistries for their superior performance characteristics.

By End-User Industry:

The end-user landscape includes Automotive, Consumer Electronics, and Energy Storage sectors. The Automotive industry accounts for the majority share, leveraging Ni5's properties for extended-range electric vehicles and performance hybrids. The Energy Storage sector is rapidly emerging as a key growth area, reflecting the global transition toward renewable energy integration and grid stabilization requirements.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/266148/global-ni-series-ternary-material-market-2024-2030-720

Competitive Landscape:

The global Ni5 Series Ternary Material market is highly competitive and innovation-driven, characterized by rapid technological advancements and strategic partnerships. The top three companies—CATL (China), LG Chem (South Korea), and Samsung SDI (South Korea)—collectively command approximately 60% of the market share as of 2024. Their dominance is underpinned by extensive intellectual property portfolios, vertically integrated production capabilities, and long-term supply agreements with major automotive manufacturers.

List of Key Ni5 Series Ternary Material Companies Profiled:

• CATL (China)

• LG Chem (South Korea)

• Samsung SDI

• Panasonic (Japan)

• Beijing Easpring Material Technology (China)

• Ningbo Ronbay New Energy Technology (China)

• Umicore (Belgium)

• BASF (Germany)

• Sumitomo Metal Mining (Japan)

• Ecopro BM (South Korea)

• Nichia (Japan)

• L&F Company (South Korea)

The competitive strategy is overwhelmingly focused on technological innovation to enhance product performance and reduce costs, alongside forming strategic vertical partnerships with automotive OEMs and battery cell producers to secure long-term demand and co-develop next-generation materials.

Regional Analysis: A Global Footprint with Distinct Leaders

• Asia-Pacific: Dominates the global market, holding a 85% share of both production and consumption. China leads this dominance with its massive battery manufacturing capacity, supported by strong government policies and complete supply chain integration. South Korea and Japan contribute advanced manufacturing capabilities and technological innovation, particularly in single crystal and high-performance variants. The region's advantage is further reinforced by its control over critical raw material processing and established export channels.

• Europe and North America: Together represent the primary demand centers outside Asia, accounting for 12% of the global market. Europe's growth is driven by ambitious EV adoption targets and local battery gigafactory construction, with numerous projects receiving significant government support. North America is experiencing rapid market expansion through the US Inflation Reduction Act incentives, which are catalyzing domestic battery material production and attracting Asian manufacturers to establish local operations.

• Rest of World: These regions represent emerging opportunities as global supply chains diversify. Countries in Southeast Asia, South America, and the Middle East are developing local battery ecosystems, though currently account for less than 3% of the global market. Long-term growth potential exists as these regions establish raw material processing capabilities and attract manufacturing investments.

Get Full Report Here: https://www.24chemicalresearch.com/reports/266148/global-ni-series-ternary-material-market-2024-2030-720

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/266148/global-ni-series-ternary-material-market-2024-2030-720

About 24chemicalresearch

Founded in 2015,has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

• Plant-level capacity tracking

•

• Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/